Finternet: The Financial system for future

Topics

- Overview of Finternet

- Problems in current financial system

- How Finternet is going to solve the problem?

- Technology deep dive on the solution

- Governance and Regulatory considerations

- Risks& Challenges

- What would be the role for Fintech in this ecosystem?

Overview of Finternet

The Finternet represents a future where financial interactions are seamless, secure, and interoperable across a global digital network.

- Interoperable financial ecosystems, with individuals and businesses positioned at the centre of their financial interactions

- Three foundational pillars.

- An economically sound architecture

- The integration of advanced technologies

- A robust regulatory and governance structure

Core principles: interoperability, verifiability, programmability, modularity,scalability, security and data empowerment

Problems in existing financial system

- Many financial transactions are delayed due to reliance on time-consuming clearing,messaging, and settlement systems, sometimes involving physical paper trails.

- Within countries, the lack of adaptive interconnectedness often results in different parts of the financial system being unable to communicate effectively.

- Cross-border transactions face even larger barriers, further complicating and delaying the process.

- ossibility of fraud due to impersonation,circumvention and compromise, bypassing established standards and protocols.

Basics of Blockchain

- We need to understand the basics of Blockchain, the underline technology on which Finternet works.

- Following concepts are explained in nutshell for better undertstanding

- Blockchain, Blocks, Mining

- How blocks are added?

- Smart contract

- Distributed ledger

- Decentralised Finance(DeFi) *Central bank digital currency(CBDC)

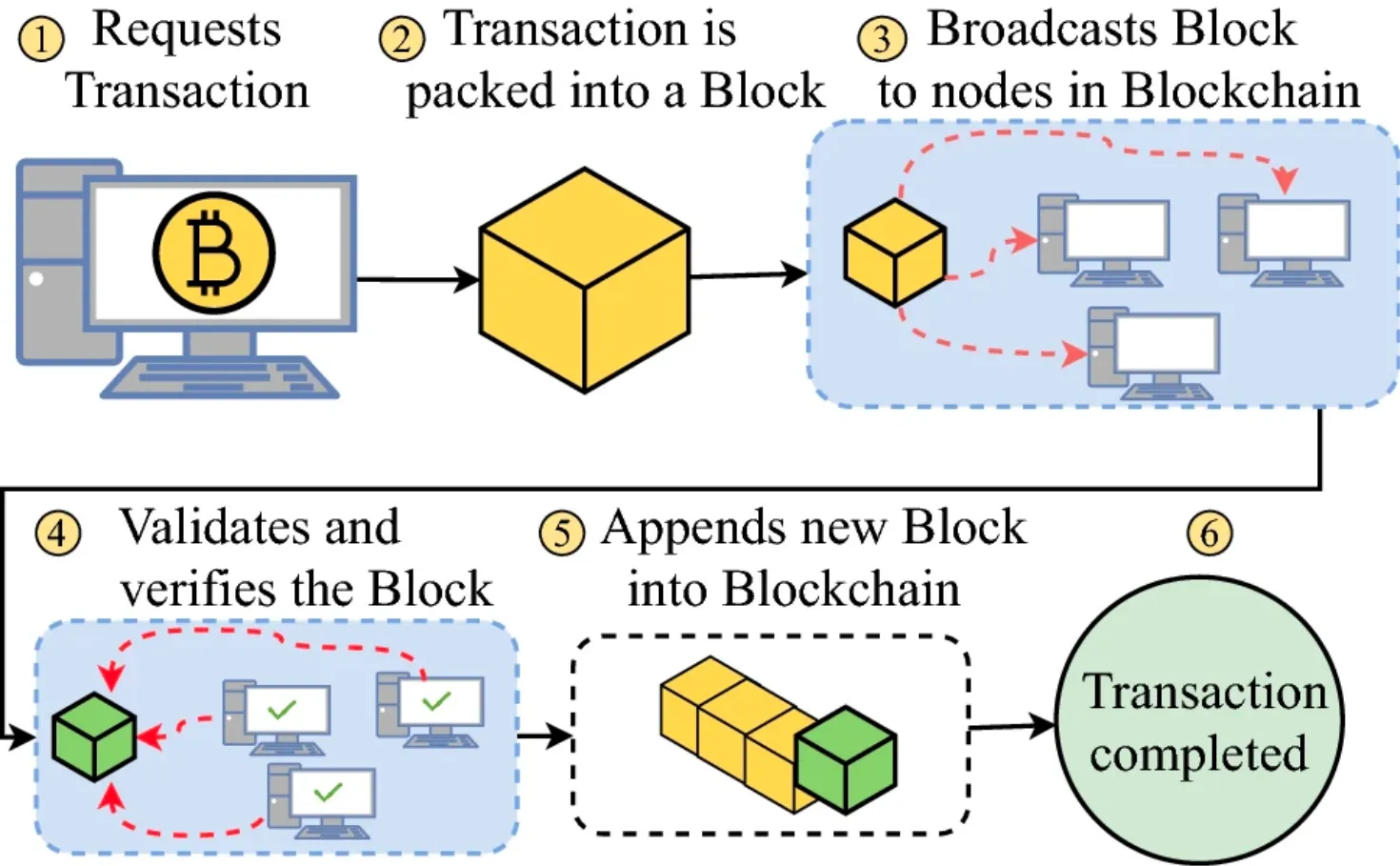

What is Blockchain?

- Block chain is a digital database or ledger that is distributed among the nodes of a peer to peer network.

- The entries created are immutable and hence no one will be able to tamper the data

- Whenever a new asset addition or update happens, blockchains store data in blocks linked together via cryptography. This is the way how each block in a block chain is stored

- Before adding a new transaction(Block) the nodes has to perform a validation or verification process by Proof of work(PoW)(or) Proof of stake(PoS). Proof of stake.

- Pls refer the link for more details

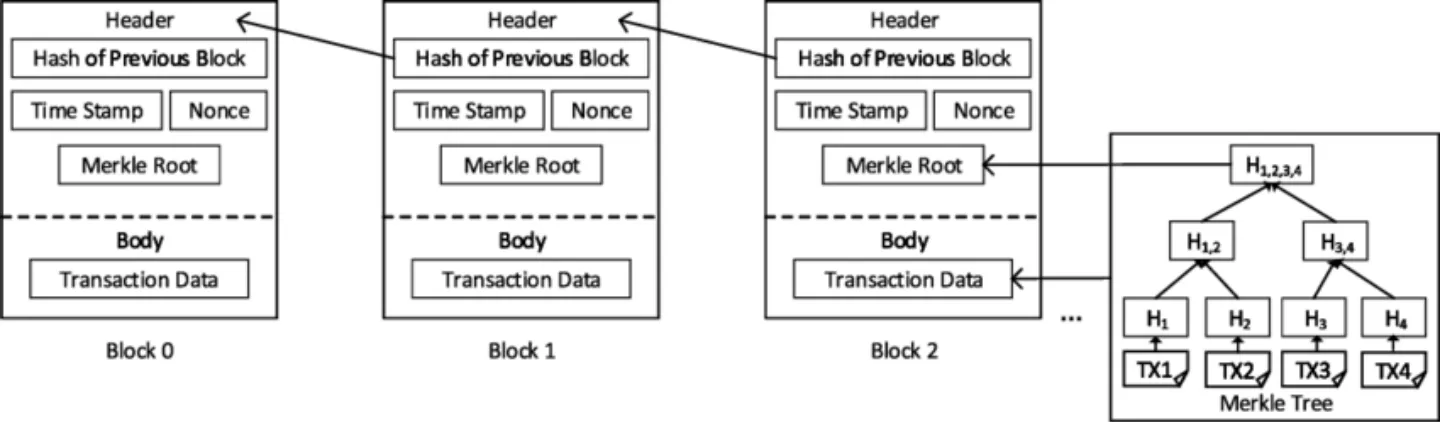

How blocks are added in blockchain?

Image Credit: Springer Link

- New transaction submitted to the Blockchain

- The transaction gets validated across the nodes in the Blockchain. Once validated, a new hash created and added to the block header

- The new block linked to the previous block’s hash in it’s header

- That’s how a chain of immutable transaction gets created

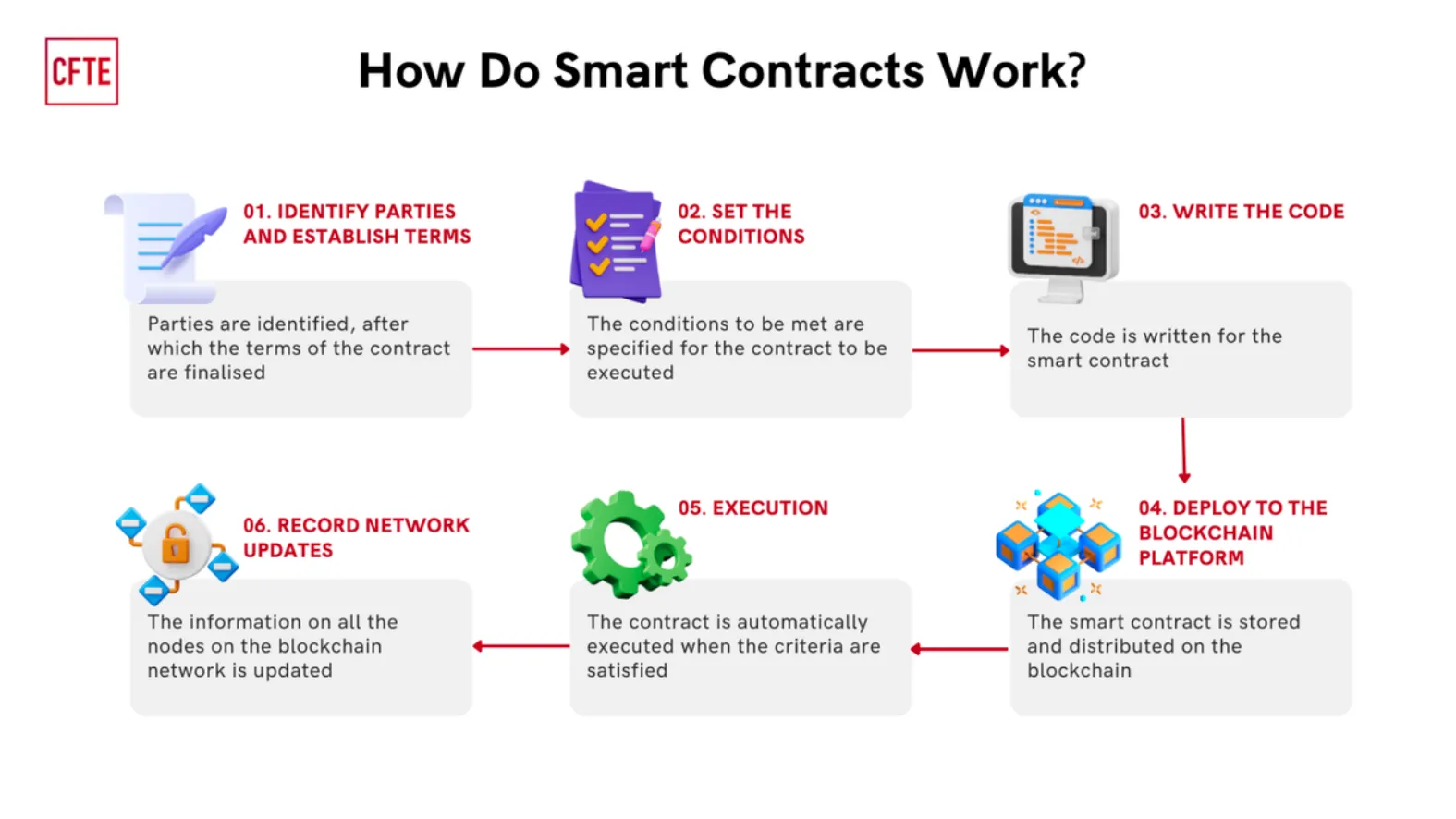

Smart contract?

Image credit:CFTE

- A smart contract is a self-executing contract in which the conditions of the buyer-seller agreement are directly written into lines of code.

- The code and the agreements contained therein exist across a distributed, decentralized blockchain network.

- Transactions are trackable and irreversible, and the code controls the execution.

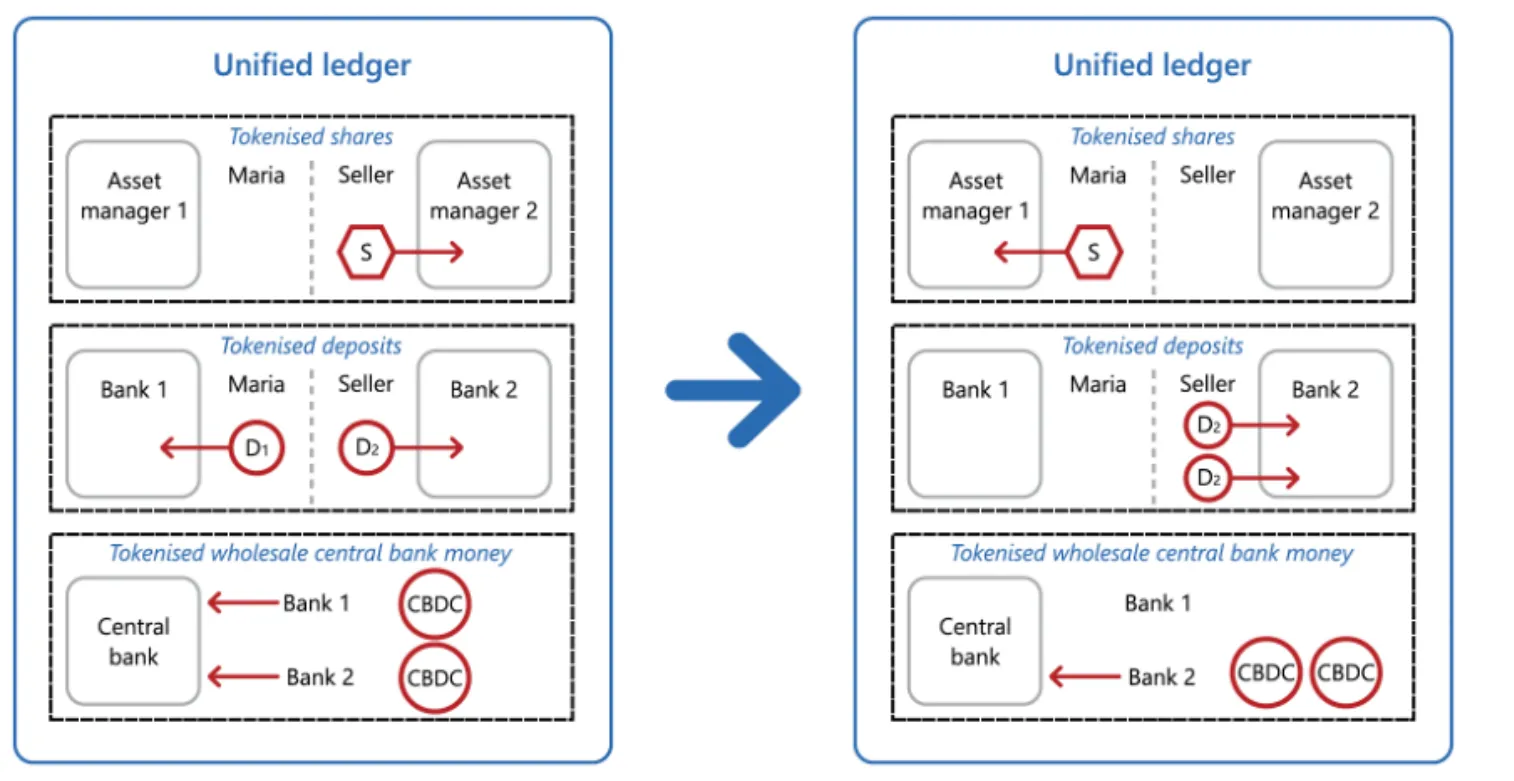

Unified ledger

- Unified ledgers provide a“common venue”(ie a shared programmable platform) where digital forms of money and other financial assets co-exist.

- Depending on the needs of each jurisdiction, multiple ledgers could coexist. The role of unified ledgers could also vary by jurisdiction

- Characteristics of unified ledger

- Single Source of Truth

- Interoperability

- Efficiency

- Transparency and Trust

- Smart Contracts

- Regulatory Compliance

It serves two purpose

- Combine all the components needed to complete financial transactions-financial assets, ownership records,rules governing their use and other relevant information-in a single venue

- Money and other financial assets exist on the ledgers as executable objects.

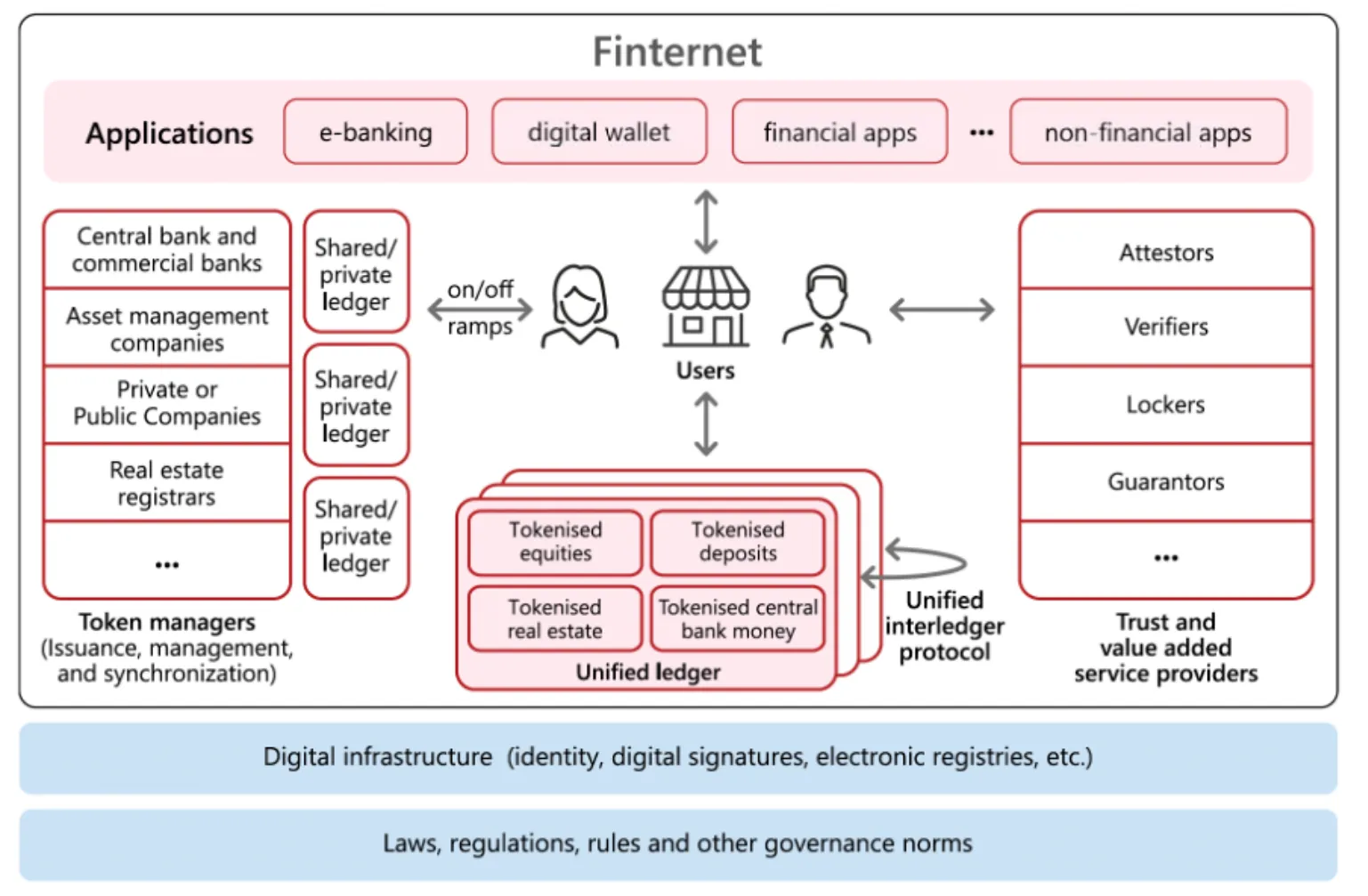

Finternet Architecture

Image Credit: BIS 2023

- Token-based financial system, supported by unified ledgers. Money and other financial assets exist on the ledgers as executable objects.

- Token managers(Banks, Insurance, Asset management companies) owns tokenizing and de-tokenizing the assets and bound by regulatory and governance.

- Individuals and businesses would interact with the ledgers through applications i.e) Existing e-banking, digital wallet, payment app etc

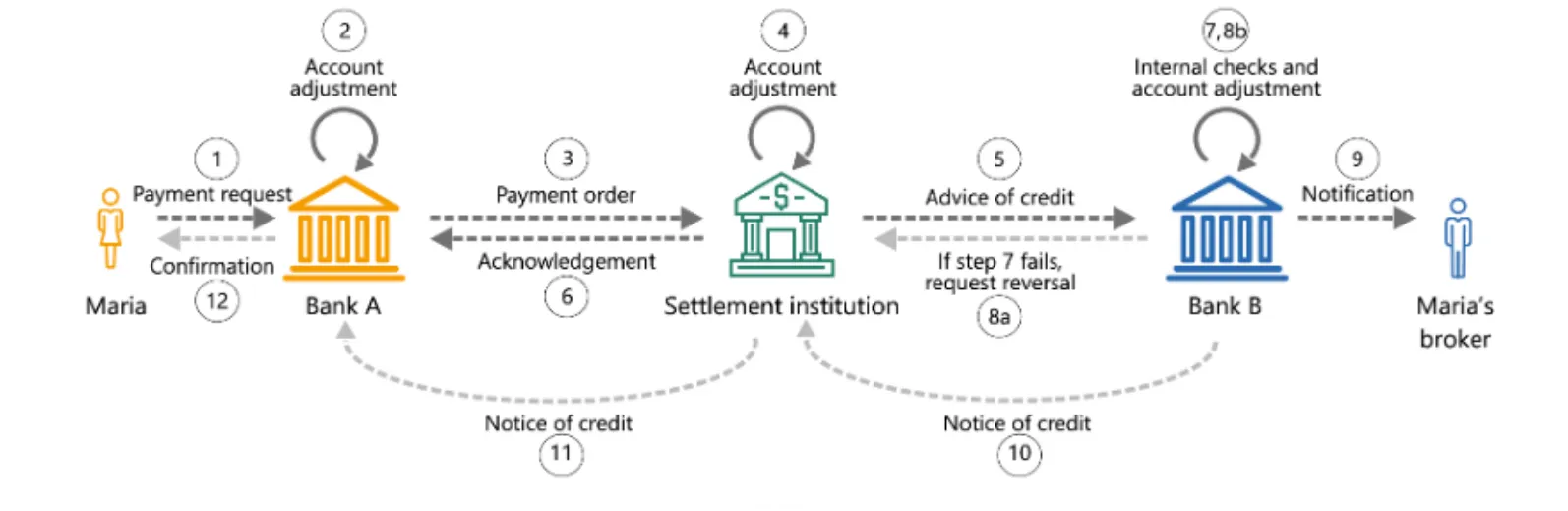

Current finance system_vs Finternet

Current finance system

Image Credit: BIS 2023

Finternet

Image Credit: BIS 2023

Finternet flow

- Maria having account with Bank1. The amount in the bank is converted to deposit tokens(D1) and stored in the unified ledger.

- Bank B1 has mapping to the corresponding central bank digital currency(CBDC) with central bank and stored in unified ledger

- Similarly Seller has relation with Bank2 with deposit token D2.

- Seller’s stock is also tokenized and stored in the unified ledger by the Asset Management company.

- When Maria intent to buy the stock from Seller,first the equivalent deposit token transferred to the seller account. Corresponding CBDC token moved to the central bank unified ledger.

- Token contains the details about the ownership etc and the contract, regulation rules etc will be executed by the smart contract without any external intervention.

- Similarly other governed assets like Real estate,Vehicle, bonds and non-governed assets like arts also can be transferred similar fashion

GovernanceRegulations

- Automating regulatory compliance and enforcement at the token level through the pivotal role of token managers. These managers are the custodians of compliance.

- Non-repudiability ensures unequivocal accountability for all actions within the ecosystem, reinforcing the integrity of transactions.

- Auditability enables rigorous verification of compliance and integrity across the board, assuring adherence to legal and regulatory frameworks.

- Observability provides stakeholders with real-time insights, facilitating swift and efficient dispute resolution and proactive issue management.

- A basic starting point is that existing laws and regulations should apply to participants and assets in the Finternet.

- Unified ledgers and related infrastructure should not provide venues to circumvent laws or to engage in regulatory arbitrage

Risk& Challenges

- Regulatory challenges

- Whether central banks have the authority to issue tokenised central bank money.

- The legal status of the tokens that exist on unified ledgers requires clarification

- Tax treatment of these assets

- Insurance cover for those deposit if the issuing bank were to fail.

- Careful examination of how existing legal requirements apply to assets that exist in a tokenised environment

- How financial institutions can participate in the ledger and decision-making regarding the types of assets and tokens that appear on the ledger and the rules governing their use.

- Is it going to be fully publicly owned and operated entities(or) Owned by private sector solutions, with public authorities role limited to establishing the overriding legal framework and enforcing basic investor and consumer protection safeguards

- Trust in the financial system does not come from technology but from the legal and regulatory framework that underpins it

- International cooperation in designing a legal and regulatory framework for unified ledgers. i.e) Cross border payments

Risk Challenges

Technology challenges

- The key advantage of blockchain is distributed ledger, but the proposed solution goes traditional with unified ledger,it raises the question on the integrity of the system

- Blockchain is energy intensive technology. Please refer the below diagram. The energy needs for deploying this solution across country like India(or) across globe is going to consume huge energy. Given that the contribution of renewable energy is 29% as on 2023 based on UN report. Is it really worth investing?

- Blockchain was considered unhackable few years before but the recent advancement made in quantum computing changes the situation. How secured this system is going to be in future?